Unlimited payment cards with a remote and hassle-free account setup process along with SEPA, FPS and SWIFT transfers

100 +destinations

7 yearsin the market

1000 +accounts opened

Cards for all your needs

A comprehensive range of payment cards, with up to 10,000 cards per month, easy card management, API integration, and top security features.

Debit Card of your choice — Virtual or Plastic

Any card purchase you make is protected by Mastercard. If there is any issue with the purchase, you can request a refund.

Card-as-a Service

Build your own card product with ease

Mass Card issuing

Whether you need 100 or up to 10,000 cards per month, we've got you covered.

Easy Card management

Use your Mastercard in the UK, online, or abroad with no hidden fees.

PCI DSS certified

Rest assured that your information is protected and has the highest level of data security with our PCI DSS certification.

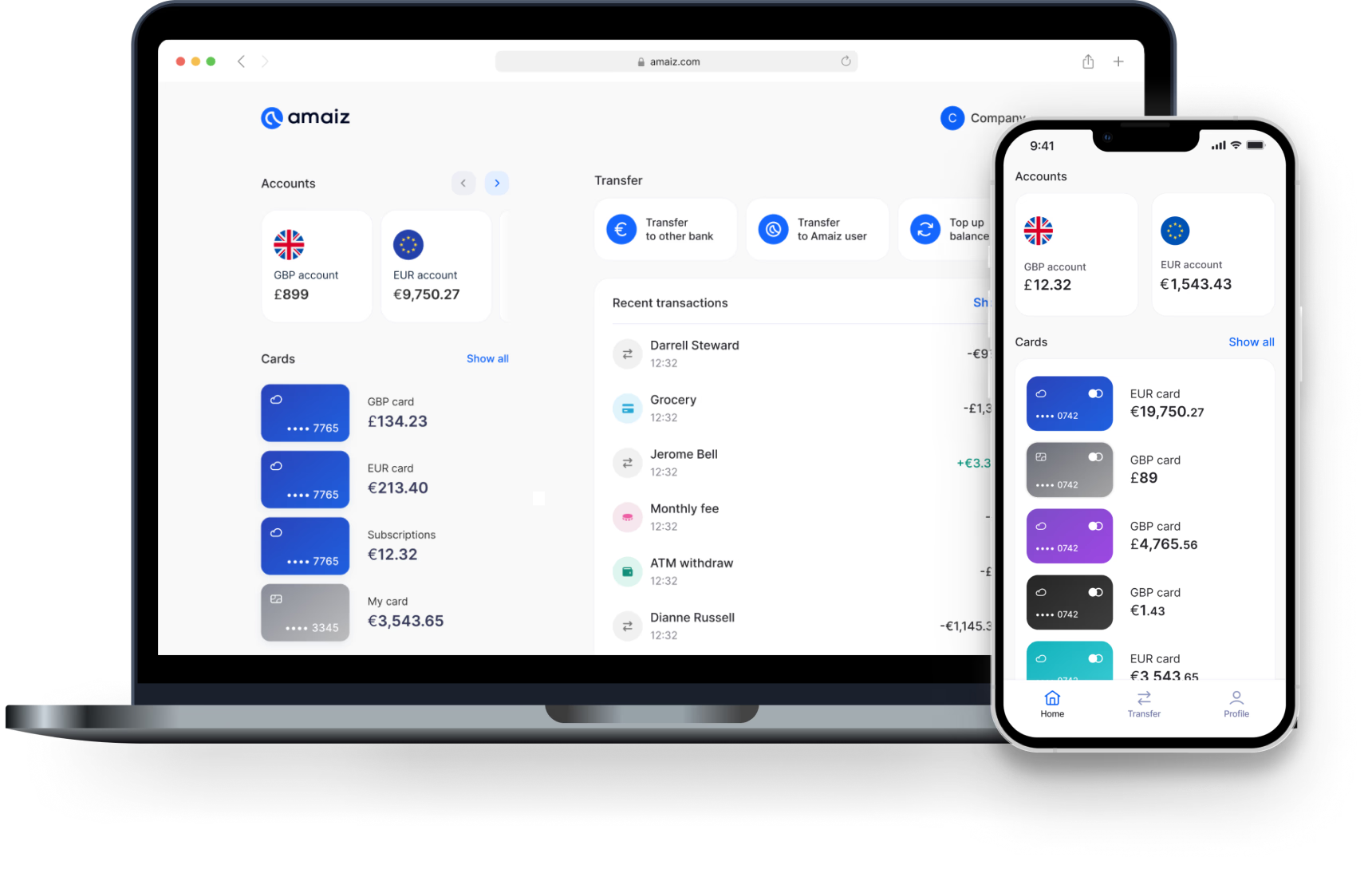

Transfer Money Worldwide

Simply complete our online application, pass the compliance check, and you'll have access to your account.

Sender country

Recipient country

Available Currency

Why choose Amaiz?

Features that transform your payments

GBP & EUR accounts

Empower your payments with a unique Sort Code and Account Number for UK payments and an IBAN for international payments.

Regulated & Secured

We follow strict FCA protocols and hold your funds in a safeguarding account to ensure your secure banking experience.

100% Digital setup

Opening an account is quick and hassle-free. Simply complete our online application, and you’ll have access to your account with no need to visit a branch.

Personalised Solution

Each customer is unique, and our banking solution is designed to meet the needs of all customers, from individuals to high-risk entities.

Try free demo account

Enter your email and we will send you a link to the demo account

Easy Account Setup

Simply complete our online application, pass the compliance check, and you'll have access to your account

1

Complete the application

Tell us about your company and the nature of your business

2

Complete KYC check

Upload all necessary corporate documents to finalise the KYC process

3

Accept pricing

After the KYC check, we will provide you with a special offer and terms

Pricing

Our pricing starts as low as £0 per month, and your fees depend on your business.

Business

Onboarding fee: Free

£0/ Month

Business +

Onboarding fee: £100

£49/ Month

Enterprise

Onboarding fee: £250 - £1000

£99/ Month

The final decision is based on your risk profile

Interested in discussing a tailored offer for your business?